What Nigeria, Ghana, Senegal, and the ECOWAS region must do before the oil revenue spike becomes another wasted opportunity and the crisis becomes a permanent condition for everyone else

I. Two Economies Living in One Region

West Africa is living through two simultaneous economic realities in the wake of the war in Iran, and the temptation to manage them as separate problems is exactly the error that will squander what this moment has created. On one side: Nigeria, sitting atop a potential oil revenue windfall of historic proportions, with its crude suddenly priced well above the budget benchmark and its Dangote Refinery positioned as the Atlantic Basin’s most significant alternative refining capacity at a moment of global refined product shortage. On the other: Ghana, Senegal, Côte d’Ivoire, and the rest of the region’s net importers, absorbing imported fuel inflation at a moment when Ghana’s three-year economic recovery was finally within reach, Senegal’s new hydrocarbon revenues were beginning to materialise, and household purchasing power across the ECOWAS region was only beginning to recover from the 2022 and 2023 commodity shocks.

The utilitarian argument for a West African collective response does not rest on solidarity. It rests on the arithmetic of shared assets. Nigeria’s refining capacity can supply West Africa’s fuel deficit. Morocco’s OCP phosphate operations can supply West Africa’s fertiliser deficit. Ghana’s financial services sector and ICT infrastructure can provide the settlement architecture. ECOWAS’s legal framework can remove the non-tariff barriers that currently prevent these transactions from happening at scale. These are not things that need to be built. They exist. What needs to be built is the political will to use them in combination, at the speed the crisis demands.

II. Nigeria: The Windfall That Must Not Be Wasted Again

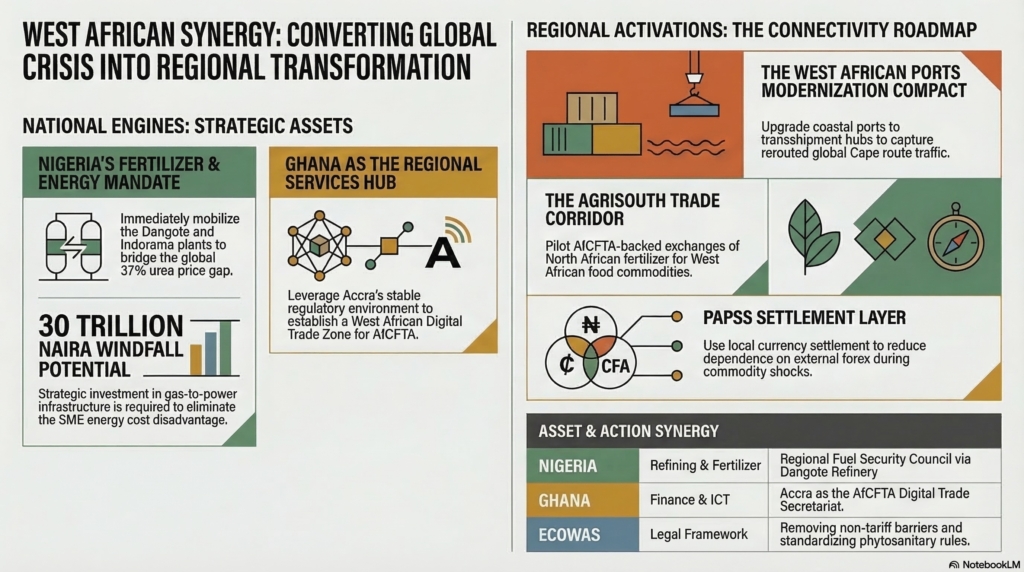

Nigeria has received oil windfalls before. The pattern that follows them is well documented across four decades of post-independence economic history: the fiscal space created by elevated prices gets absorbed by recurrent expenditure, subsidy commitments that prove impossible to unwind, elite capture of revenue distribution mechanisms, and the institutional entropy of a federation whose allocation system was designed for a different era. The NESG estimates suggest windfalls ranging from 2.3 trillion naira under a short conflict to thirty trillion naira if the war becomes protracted. The question is not whether those revenues will arrive. It is whether they will be used to change anything structural, or whether Nigeria will emerge from this crisis with slightly fuller coffers and exactly the same vulnerabilities it entered with.

Nigeria has received oil windfalls before. The question is not whether the revenues will arrive. It is whether Nigeria will use them to change anything structural, or whether it will emerge from this crisis with slightly fuller coffers and exactly the same vulnerabilities it entered with.

The structural constraint on the windfall is significant. Nigeria’s actual output runs approximately 20% below its own budget projection — roughly 1.48 million barrels per day against a budgeted 1.84 million — because security challenges, pipeline vandalism, and crude theft continue to limit production ramp-up capacity. The Dangote Refinery, operating at 650,000 barrels per day, still requires imported heavier crude grades for blending that Nigeria does not produce domestically, so when global crude prices rise, Dangote’s input costs rise too, partially offsetting the gain. Nigerian citizens are already paying close to 1,400 naira per litre for petrol, as deregulated domestic prices track global markets upward in a country where most businesses run on diesel generators because the national grid cannot be trusted.

The fertiliser opportunity Nigeria is currently squandering

The most consequential thing Nigeria can do for the continent right now is not to manage its oil revenues carefully. It is to immediately mobilise the Indorama urea plant and the Dangote Fertiliser facility as emergency suppliers to food-insecure countries across West and East Africa, through AfCFTA-facilitated channels, at the exact moment when Gulf fertiliser suppliers have suspended contracts and urea prices have risen 37% in a week.

This is not a hypothetical future option. Both facilities are operational. The AfCFTA framework already provides for preferential treatment on agricultural inputs. Afreximbank offers commodity trade finance instruments. PAPSS provides the local currency settlement layer. What is required is a ministerial decision — this week, not next quarter — to activate these instruments in combination and to publicly announce the terms on which Nigeria will supply fertiliser to ECOWAS member states and beyond. The commercial logic is compelling. The political logic is transformative. A Nigeria that steps into the Gulf fertiliser gap and supplies urea to Senegalese farmers, Ghanaian smallholders, and Ivorian cocoa producers is demonstrating, in the most concrete way possible, that intra-African trade serves African welfare — and is building supply relationships that will outlast the crisis.

Dangote as a regional energy security anchor

The Dangote Refinery is the largest single-train refinery in the world. At a time when global refined product supply is disrupted and Atlantic Basin buyers are scrambling for alternatives, it is well positioned to be a genuine regional and global refining hub — not merely a domestic fuel supplier. Dangote’s CEO has already signalled interest in European supply. The Nigerian Foreign Ministry is positioning Nigeria as a strategic diversification partner for Gulf buyers.

The proposal: Nigeria should convene a West African Regional Fuel Security Council — Nigeria, Ghana, Senegal, Côte d’Ivoire, and the ECOWAS Secretariat — with a mandate to negotiate a regional petroleum supply agreement giving member states preferential access to Dangote’s output, financed through PAPSS, at a price formula tied to Brent crude rather than the volatile spot market. This converts a national industrial asset into a regional energy security infrastructure in a single institutional move. It also gives Nigeria leverage to demand reciprocal market access for Nigerian-manufactured goods in countries currently served by Asian and European suppliers.

What the windfall must build

The most important investment the current oil revenue windfall could make is one that compounds across every sector: eliminating the energy cost disadvantage that makes Nigerian manufacturing structurally uncompetitive. A Nigerian SME running on a diesel generator pays three to four times the energy cost of a comparable firm in Morocco, Vietnam, or Turkey. That differential is not a productivity problem, a skills problem, or a market access problem. It is an infrastructure failure, and it is solvable with capital at the scale that thirty trillion naira creates. Gas-to-power infrastructure, grid stability investment, and the regulatory reforms that would allow independent power producers to operate and compete: these are the investments that convert a windfall into a structural transformation rather than a budget cycle.

III. Ghana: Protecting the Recovery and Capturing the Opportunity

Ghana’s return to 3.3% inflation by February 2026, from a peak of 54.1% in December 2022, is among the most difficult macroeconomic achievements in Africa in recent years. It required the IMF programme, painful fiscal adjustment, and a population that absorbed three years of compressed purchasing power while the government rebuilt its credibility. That recovery is now directly threatened by an externally driven commodity shock that Ghana’s domestic monetary policy cannot address. The Bank of Ghana faces a genuinely difficult choice between tightening to defend the cedi and cutting to support the recovery. The recommendation here is to accept a temporary, modest inflation overshoot rather than raise rates in response to supply-side price pressures that monetary tightening cannot resolve.

Ghana spent three years rebuilding from 54% inflation through painful fiscal adjustment and compressed household purchasing power. The Iran war threatens that recovery through a channel Ghana cannot control. The correct response is not to let the IMF programme metrics determine monetary decisions designed for a different problem.

The more productive policy response is on the fiscal and strategic side. Ghana’s GANRA gold reserve accumulation programme, in a gold-price environment above $5,400 per ounce, is generating reserve growth that provides a stabilisation buffer. That buffer should finance targeted fuel subsidies for the most vulnerable households — not as a permanent commitment but as a time-limited shock absorber — without blowing the fiscal deficit that the three-year recovery effort rebuilt.

Ghana as West Africa’s services and fintech hub

Ghana’s ICT sector grew 28.3% year-on-year in late 2025. This is the fastest-growing sector in West Africa by some measures, and it provides a structural buffer against commodity shocks that Nigeria, with its greater oil dependence, lacks. Ghana has the human capital, the regulatory environment, and the digital infrastructure to position itself as the services hub of West Africa — at a moment when ECOWAS’s commodity exporters are generating revenues that require sophisticated financial services, the Cape route is creating new trade finance demand, and the AfCFTA’s digital trade protocol is being written with its architecture still undefined.

Ghana should table, at the next ECOWAS summit, a proposal for a West African Digital Trade Zone, establishing Accra as the operational headquarters of the region’s AfCFTA digital trade secretariat and designating Ghanaian fintech firms as the preferred settlement layer for PAPSS transactions across the ECOWAS corridor. This is not generosity. It is the strategic capture of a position that is available right now, before Lagos, Abidjan, or Dakar makes competing claims. Lagos is the larger economy; Accra has the more stable regulatory environment and the more trusted financial system. Ghana should use that advantage aggressively and explicitly.

IV. The ECOWAS Activations

West African ports as a Cape route network

The Atlantic coast of West Africa — Dakar through Abidjan, Tema, Lagos, and Douala — sits directly on the Cape route, which now carries two-thirds of global shipping. None of these ports is currently positioned as a major transhipment hub, bunkering centre, or maritime service facility at the scale the rerouted traffic demands. The opportunity is both commercial and strategic, and it requires coordinated investment rather than each port competing independently for the same ships.

The ECOWAS proposal: a West African Ports Modernisation Compact, a coordinated investment programme financed through African Development Bank infrastructure bonds, Afreximbank trade finance, and sovereign co-investment, that upgrades at minimum two West African ports to full transhipment capability within three years. The model is Tanger Med in Morocco — built from a greenfield site to a top-twenty global container port in a decade through exactly this combination of coordinated sovereign and multilateral investment. There is no geographic reason why Dakar, Tema, or Lagos cannot replicate that trajectory. There are institutional and political reasons that are, in principle, changeable.

The AgriSouth corridor: making AfCFTA’s agricultural chapter work in practice

West Africa grows food that North Africa needs — maize, cowpeas, groundnuts, and palm oil. North Africa produces fertiliser that West Africa needs — urea and phosphate from Morocco and Egypt. The AfCFTA agricultural trade chapter provides the tariff framework to make this exchange routine and affordable. It is not operational at scale due to non-tariff barriers, incompatible phytosanitary standards, and the lack of trade finance instruments accessible to smallholder producers and small trading firms.

The utilitarian action: launch a West Africa-North Africa agricultural trade pilot covering these specific commodities, financed through Afreximbank instruments, settled through PAPSS, and tracked publicly so that African businesses and governments can see the price differential between intra-African supply and external alternatives. When the data show that Moroccan urea is landing in Kano more cheaply through AfCFTA channels than through spot-market procurement from Asia, the political case for investing in the corridor infrastructure becomes self-evident. You cannot argue people into structural change. You can show them the price difference and let the market argument make itself.

V. The Utilitarian Test

The utilitarian case for West African action is the most straightforward on the continent, because West Africa has both the assets and the institutional framework to act. Nigeria’s oil and fertiliser production capacity, Ghana’s gold and financial services sector, Morocco’s phosphates, Senegal’s emerging gas production, and the ECOWAS legal framework together constitute a resource and institutional base that, managed with strategic intelligence, could convert the Iran war’s disruption into a durable repositioning of West Africa in the global economy.

That repositioning does not require waiting for the war to end, for the Hormuz to reopen, or for a new global order to emerge. It requires decisions — some of which can be made in ministerial offices this week — to treat the AfCFTA as the emergency instrument it was always designed to be rather than the aspirational framework it has been allowed to remain. The test is not ambitious. It is execution at the speed that the crisis demands.