Specific proposals for Kenya, Uganda, Tanzania, Rwanda, and the Northern Corridor — grounded in what is already available and what is inexcusably overdue

I. The Paralysis That Cannot Afford to Continue

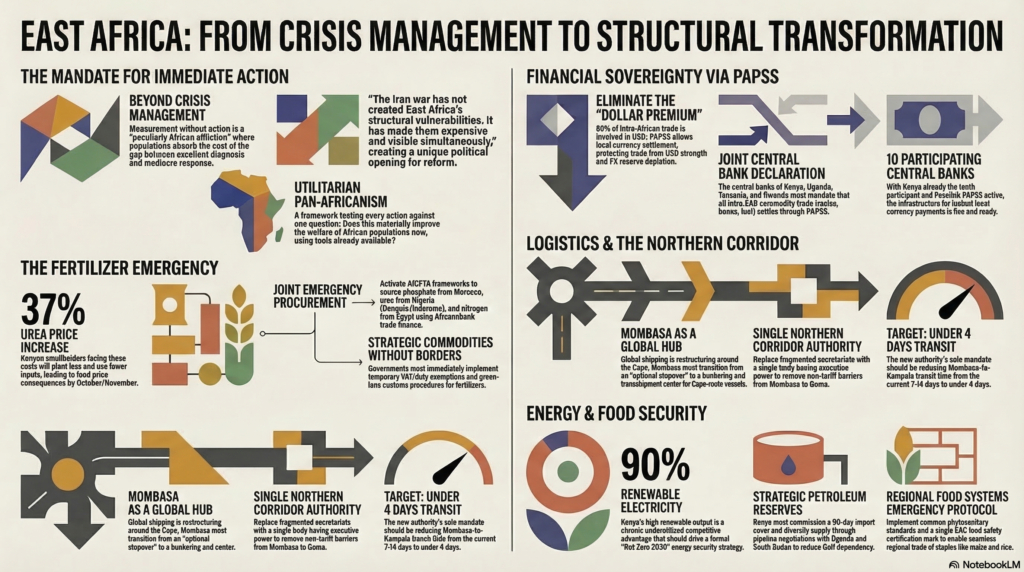

East Africa entered this crisis in a structurally vulnerable position, and the analysis produced since the strikes has, predictably, focused on quantifying that vulnerability. The import bill. The fuel reserves. The fertiliser shortfall. The shipping delays. The second-round food price effects. All of that analysis is necessary, and most of it is correct. But measurement without action is a peculiarly African affliction — the continent’s policy ecosystem produces excellent diagnoses and mediocre responses, and the gap between them is where populations absorb the cost.

I want to argue for something more demanding than crisis management. The Iran war has not created East Africa’s structural vulnerabilities. It has just made them both expensive and visible. That combination — expensiveness plus visibility — is the precise condition under which structural change becomes politically possible. The question is whether the governments of Kenya, Uganda, Tanzania, Rwanda, and their private sectors can act on that possibility before the news cycle shifts and the urgency dissipates.

The Iran war has not created East Africa’s structural vulnerabilities. It has made them both expensive and visible. That combination is the precise condition under which structural change becomes politically possible.

The framework I am operating from is the one I have developed over the past several years: a utilitarian Pan-Africanism that tests every proposed regional action against a single question — does this materially improve the welfare of African populations, now, through the most aggressive possible use of the tools and institutions already available? Not eventually. Not when the 54-country consensus arrives. Now.

II. The Fertiliser Emergency: Act Before the Planting Window Closes

Kenya’s long rains planting season is open. Farmers across the maize belt are making decisions about inputs at this moment — not after the trade ministers have met, not after the EAC Secretariat has circulated a draft framework. Now. A Kenyan smallholder who cannot afford urea at 37% above last season’s price will plant less, use fewer inputs, and harvest less. The food price consequences arrive in October and November, six months after the headlines have moved to the next crisis.

The required emergency action is as follows, and it should have happened two weeks ago. Kenya, Uganda, and Tanzania should immediately activate a joint emergency fertiliser procurement through the AfCFTA framework. The suppliers exist on the continent: Morocco’s OCP is the largest phosphate producer on earth; Nigeria’s Dangote Fertiliser facility and the Indorama urea plant are operational and supplying the continent; and Egypt’s nitrogen production can partially substitute for disrupted Gulf urea. Afreximbank offers trade finance instruments that can back letters of credit for sovereign-level commodity purchases. The AfCFTA framework already provides for preferential treatment on agricultural inputs.

The IFDC, SUSTAIN Africa, and AfricaFertilizer have publicly called for governments to treat fertilisers as strategic commodities without borders, with temporary VAT and duty exemptions and green-lane customs procedures. The EAC agriculture ministers should convene — not in three weeks, but this week — not to deliberate but to announce. The announcement should be specific: which suppliers, which volumes, which financing mechanism, which delivery timeline, which border facilitation protocol. Anything short of that level of specificity is a communiqué, and communiqués do not feed crops.

A Kenyan smallholder who cannot afford urea at 37% above last season’s price will plant less and harvest less. The food price consequences arrive in October, six months after the headlines have moved on. The emergency exists now.

III. Activate PAPSS as the Regional Settlement Layer

Kenya is the tenth central bank to participate in the Pan-African Payment and Settlement System. The Pesalink-PAPSS partnership, activated in February 2026, enables instant cross-border payments in local currencies. The infrastructure is live. The policy action required to make it consequential is simple and available: the Central Bank of Kenya, the Bank of Uganda, the Bank of Tanzania, and the National Bank of Rwanda should issue a joint declaration that all intra-EAC commodity trade — fertiliser, maize, beans, palm oil, refined petroleum products — will settle in local currencies through PAPSS, with dollar conversion required only at the point of final external trade settlement.

The welfare logic is direct. Over 80% of intra-African trade is currently invoiced in US dollars. When the dollar strengthens — as it does during every global risk event, including this one — the cost of African-to-African trade rises in local-currency terms, even when no actual dollar transaction is involved. The trader in Kampala buying Kenyan beans is paying a dollar premium on a transaction that has nothing to do with the United States. PAPSS eliminates that premium. At a time when East African currencies are under pressure, and foreign exchange reserves are being drawn down to service elevated import bills, reducing the dollar intermediation cost in intra-regional commerce is not an ideological choice. It is fiscal arithmetic.

IV. Mombasa Must Decide What It Is

The rerouting of global shipping around the Cape is not a temporary emergency measure. The combination of Hormuz closure and Red Sea risk has fundamentally repriced alternative maritime routes. Carriers are not making these decisions on a voyage-by-voyage basis — they are restructuring their service networks. Maersk and Hapag-Lloyd have already announced structural rerouting rather than temporary diversions. This reconfiguration will persist well beyond the resolution of the immediate Iran conflict, because war-risk insurance and shipper risk calculations are slow to reverse.

Mombasa sits at the intersection of the Indian Ocean trade lane and the East African hinterland. It is the natural transhipment hub for landlocked Uganda, Rwanda, Burundi, South Sudan, and eastern DRC. It is positioned — geographically — to be a bunkering and maritime services centre for Cape-route vessels. It is not currently performing any of these functions at a competitive scale, and the reason is institutional.

The Kenya Ports Authority and the Kenya Maritime Authority need to jointly declare a Maritime Emergency Investment Programme, with a specific twelve-month mandate and public performance targets. The mandate should cover four things: cold storage expansion for horticultural re-export; a bunkering facility capable of servicing Cape-route vessels; a minimum of three global shipping line agreements making Mombasa a scheduled port of call rather than an optional stopover; and the licensing of port-adjacent processing zones that can add value to East African agricultural products before onward export via the Cape route.

Mombasa has everything it needs to be a serious Indian Ocean logistics hub except the institutional decision to be one. Geography, hinterland connectivity, and the Cape route surge have provided the moment. The port authority and the maritime regulator have to decide whether to use it.

The financing is available. The African Development Bank has mandates for maritime infrastructure. Afreximbank has trade facilitation instruments. What has been missing is a government-level declaration that Mombasa is a continental strategic asset and will be treated as such, with the licensing speed, regulatory clarity, and capital mobilisation that such a distinction demands. The war in Iran has created the political moment for that declaration. It will not stay open indefinitely.

V. The Northern Corridor Must Have a Single Accountable Operator

The Northern Corridor — Mombasa through Nairobi to Kampala, Kigali, Bujumbura, and Goma — carries approximately 80% of the landlocked countries of East and Central Africa’s import and export trade. It is also a corridor of institutional fragmentation: multiple secretariats, inconsistent transit bond requirements, weighbridge delays, and border formalities that, in practice, add days to transit times and impose costs that function as a tax on intra-African trade that no negotiating table has the mandate to address.

The proposal is specific and deliberately challenging: appoint a single Northern Corridor Authority, with executive power to remove non-tariff barriers along the entire length of the corridor, staffed jointly by the five member countries and financed through a modest levy on corridor transit volumes. Give it a three-year mandate and one performance target: reduce average Mombasa-to-Kampala transit time from the current seven to fourteen days to under four days. Publish the data quarterly. If it does not perform, replace the leadership.

Under AfCFTA rules, the goods moving along this corridor are already eligible for preferential tariff treatment. The barrier is not tariffs. It is time. A unified corridor authority with executive, rather than advisory, powers and a published performance mandate is the institutional form that time reduction requires.

VI. Kenya’s Energy Security Must Become a Strategic Priority

Kenya’s dependence on Gulf petroleum — over 80% of its refined product imports — is its most direct and most structurally urgent exposure to the current crisis. It will recur with every future Gulf disruption unless it is addressed at the root. The response has two components that must be pursued simultaneously.

On import diversification

the government should immediately open government-to-government negotiations with Uganda and South Sudan to secure refined product supply via pipeline infrastructure, recognising these as medium-term investments that require refinery development. Simultaneously, Kenya must commission a strategic petroleum reserve that provides at least 90 days of import cover — compared to the critically low buffer confirmed by the Cabinet Secretary’s April deadline statement. The G-to-G arrangement with Saudi Aramco, ADNOC, and ENOC is a genuine buffer only as long as physical supply moves. When the Strait of Hormuz closes, that arrangement provides credit terms on oil that is not arriving.

Kenya already generates approximately 90% of its electricity from renewable sources. This is a structural advantage that has been chronically underutilised as a strategic and commercial message. The country should formally declare a net-zero energy economy target by 2030 and build the grid infrastructure to back that declaration — not as an environmental commitment for international consumption, but as an explicit energy security strategy that reduces the import bill, eliminates the vulnerability the current crisis has exposed, and provides a competitive cost advantage for Kenyan manufacturing. These are the same arguments.

Kenya already produces over 90% of its electricity from renewables. That is a remarkable achievement that has been treated as a line in a development report rather than as a competitive advantage and a foreign policy asset. The Iran war is the moment to change that treatment.

VII. The Regional Food Systems Architecture

East Africa grows the food it needs. Uganda produces maize surpluses in good years that Kenya needs in bad ones. Tanzania grows rice that Rwanda could buy more cheaply than it currently imports. Kenya’s highlands produce tea, coffee, and horticultural crops that could supply markets in Ethiopia and the DRC at prices and lead times competitive with those of Asian suppliers — if the logistics were in place. The intra-regional food trade that would make all of these exchanges routine is currently obstructed by non-tariff barriers, incompatible phytosanitary standards, road transport costs that add 45% or more to the retail price of goods moved across borders, and payment systems that impose dollar intermediation on transactions that involve no dollars at all.

The EAC needs to declare a Regional Food Systems Emergency Protocol and implement it at COVID-era speed: a common phytosanitary standard for staple crops; a single EAC food safety certification mark enabling a Ugandan grain trader to access Kenyan and Tanzanian markets with one inspection; and a collective regional food reserve held at designated border warehouses, accessible to member states on agreed terms. The modelling has been done. The frameworks have been published. The question is whether ministers will sign the instruments before the next harvest cycle begins — or wait until the food price data from late 2026 forces the conversation under much greater political pain.